The Statement of Changes in Equity is a fundamental financial document that provides insight into how a companies equity evolves over a given period. While many investors primarily focus on the income statement, balance sheet, and cash flow statement, the statement of changes in equity offers a unique perspective on how a company manages its profits, dividends, and share capital. It essentially acts as a bridge, linking the companies profitability to its financial position by showing how retained earnings, shareholder distributions, and other factors impact equity. For investors, understanding this statement is crucial to evaluating how well a company allocates resources to create long-term value.

Equity, in a corporate context, represents the shareholders ownership interest in the company. It is calculated as the difference between total assets and total liabilities. The statement of changes in equity illustrates how this ownership stake changes from one reporting period to the next. These changes can result from the companies operating performance, dividend payouts, share issuances or repurchases, and other comprehensive income items. Unlike the income statement, which focuses solely on profitability, or the balance sheet, which provides a snapshot of financial standing at a particular moment, the statement of changes in equity reveals the ongoing adjustments that reflect the companies evolving financial strategy.

Understanding the importance of this statement requires an appreciation of the insights it provides about a companies financial behavior. For investors, it answers several critical questions: Is the company reinvesting its earnings to fuel growth, or is it distributing profits to shareholders as dividends? Is the business raising new capital through share issuance, or is it repurchasing shares to consolidate ownership? Are there significant gains or losses recorded in other comprehensive income that could affect the companies net worth without appearing in the income statement? By examining these elements, investors can better evaluate a company’s financial management practices and the sustainability of its growth.

AAPL.US

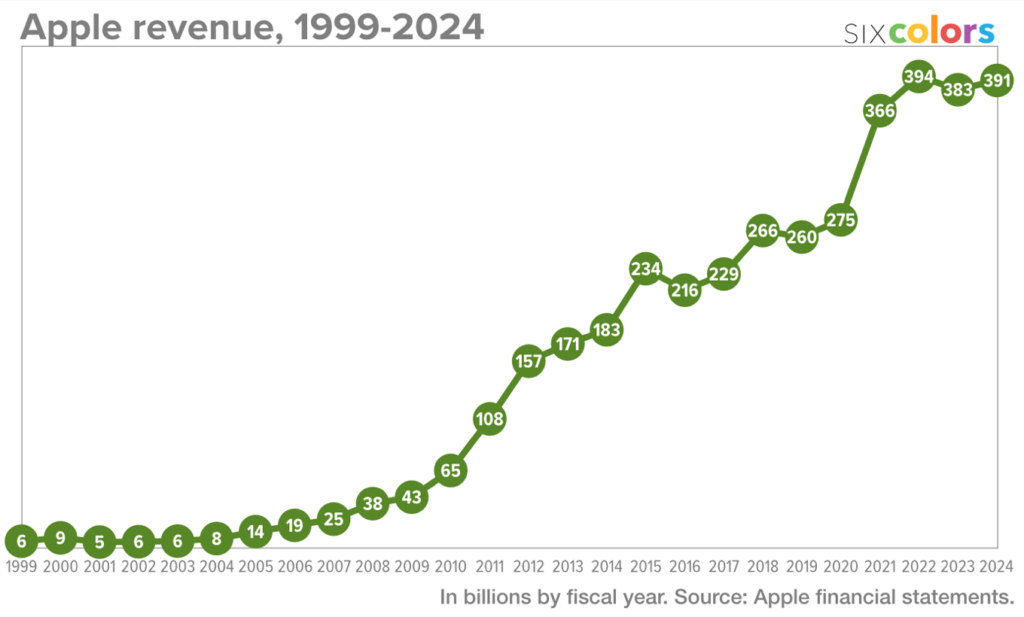

To illustrate this concept more concretely, consider the case of Apple Inc., one of the world most prominent technology companies. Apple, like many other publicly traded corporations, publishes a statement of changes in equity as part of its annual and quarterly reports. Examining Apple equity changes over time reveals how the company has consistently balanced profitability, shareholder returns, and capital structure adjustments to maintain its market leadership.

Apple financial history demonstrates a remarkable capacity to generate substantial profits while returning significant value to shareholders. In a typical year, Apple statement of changes in equity shows robust growth in retained earnings, reflecting its consistently high net income. For example, in its fiscal year 2023 report, Apple recorded tens of billions of dollars in net income, contributing significantly to retained earnings. This growth in retained earnings indicates that Apple not only generates profits but also retains a portion of those earnings to finance future innovations, product development, and global expansion efforts.

However, Apple statement also highlights substantial dividend payments. The company has maintained a steady dividend policy since it resumed dividends in 2012, regularly distributing billions of dollars to its shareholders. In addition to dividends, Apple has been particularly active in share repurchase programs. The statement of changes in equity often shows substantial reductions in share capital due to buybacks. These buybacks reduce the number of outstanding shares, thereby increasing earnings per share (EPS) and signaling management s confidence in the companies long-term prospects.

Another noteworthy aspect of Apple statement of changes in equity is the presence of items recorded under Other Comprehensive Income (OCI). OCI captures gains and losses not realized through daily operations but still relevant to shareholders equity. For Apple, these might include foreign currency translation adjustments or gains and losses related to hedging activities. While such items do not affect net income directly, they can significantly influence the companies equity position when aggregated over time.

Reading and interpreting Apple statement of changes in equity requires an understanding of how these various elements interact. The opening balance of shareholders equity at the beginning of the fiscal year sets the stage for analysis. Apple substantial net income typically contributes positively to this balance, while dividend payments and share buybacks act as deductions. Any gains or losses recorded in OCI further adjust the final equity figure. The closing balance of equity at the end of the year then provides a clear measure of how the companies financial standing has evolved.

For investors, the significance of these equity changes extends beyond the mere numbers. Apple consistent dividend payments and aggressive share buybacks reflect a shareholder-friendly policy, suggesting that the company prioritizes returning capital to investors. At the same time, the steady increase in retained earnings signals confidence in the companies future growth and ongoing innovation efforts. Such insights, gleaned from the statement of changes in equity, can help investors assess whether Apple’s financial management aligns with their investment objectives.

Interpreting this statement accurately also involves caution, as certain pitfalls can distort the apparent financial health of a company. One common error is overlooking changes in retained earnings that arise from accounting adjustments rather than genuine operational performance. For instance, if a company adopts a new accounting standard, the reported retained earnings might change significantly without any corresponding shift in actual profitability. Similarly, gains or losses recorded in OCI can sometimes mask underlying trends in net income, especially if they stem from volatile market factors like currency fluctuations or derivative valuations.

Comparing the statement of changes in equity with other financial documents provides additional context. For example, the net income figure reported in the equity statement should match the income statements net income. Similarly, the closing equity balance should align with the shareholders equity reported on the balance sheet. Cross-referencing these statements helps investors verify the accuracy of reported figures and ensures consistency in financial reporting The relevance of the statement of changes in equity varies across industries, with sector-specific differences influencing equity movements. In technology companies like Apple, retained earnings often grow substantially due to high reinvestment in research and development. In contrast, utility companies, known for their stable and predictable operations, may exhibit more consistent dividend payments and less aggressive equity changes. Recognizing these patterns helps investors interpret the statement of changes in equity within the appropriate industry context.

Moreover, accounting policies and standards can significantly impact equity figures. Changes in revenue recognition rules, for instance, might alter the reported net income and, consequently, retained earnings. Applefinancial reports often include detailed notes explaining such adjustments, ensuring that investors can accurately interpret the underlying reasons for equity changes. By paying attention to these notes, investors gain a deeper understanding of how accounting practices affect reported equity.

Ultimately, the statement of changes in equity serves as more than just a numerical record; it provides insight into a companies strategic priorities and financial discipline. For long-term investors, analyzing this statement alongside the income statement, balance sheet, and cash flow statement offers a more holistic view of the company financial performance. In the case of Apple, the statement reveals a company that successfully balances growth, profitability, and shareholder returns, reinforcing its position as a reliable investment for many.

In conclusion, the Statement of Changes in Equity is a vital, though often underappreciated, component of a companies financial reporting. It provides transparency into how profits are allocated, dividends are distributed, and share capital is adjusted. For investors, mastering the interpretation of this statement can unlock deeper insights into a companies operational efficiency, financial strategy, and long-term growth potential. Apple financial history exemplifies how effective equity management can support both innovation and shareholder satisfaction. As investors seek to make informed decisions, incorporating the statement of changes in equity into their analysis can significantly enhance their understanding of a company financial trajectory.

{kind=link}

{kind=link}

{kind=link}